Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

Seller financing lets buyers acquire businesses by paying part upfront and the rest over time with interest, making deals more accessible when traditional lending is limited. It expands buyer pools and can help sellers achieve higher overall sale value with ongoing income.

Looking for financing support for your next deal? Access Flippa’s vetted network of lending and finance partners.

Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

400,000+ Weekly Active Buyers

20+ Multi-language Brokers

Seamlessly Negotiate and Receive Offers

Integrated Legal, Insurance, Finance and Payments

Many buyers of businesses are looking to invest in businesses which they can afford to purchase outright, even if this involves short-term Earn-out agreements, which typically are not arranged primarily for finance shortfall reasons.

However, many of those looking to build a portfolio of businesses or looking to acquire a seriously high-value business may need to source finance.

Traditional business loans from banks and other major lenders are difficult to obtain for business investment. Currently, banks are highly risk-averse and even when lending for more conventional business purchases they will be restricting lending to home equity based loans.

Amazingly, after all these years of online business progress, the major banks still tend to be out of their lending comfort zones in the business website world, not really understanding or being confident about the way it operates. One of their main reasons for securing the loan with home equity is that banks cannot secure the loan against the physical assets of an online business and they are reluctant to place a value on ‘goodwill’ or business profitability potential.

We’ll cover SBA loans in a future blog post where the situation is entirely different.

Unsecured loans from small business loan specialists, including online lenders, are more readily available but generally come with unattractively high interest rates and often burdening fee structures. Private equity firms which finance online business acquisitions tend to be interested only at high-value levels, and with lots of strings attached including an intrusive degree of business control or oversight.

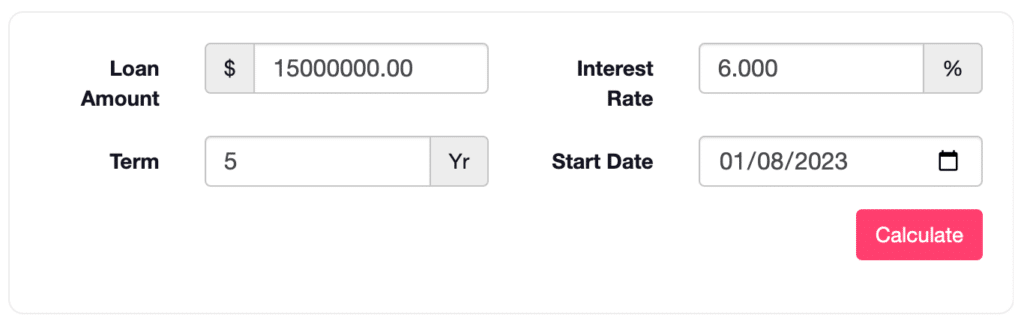

How to Calculate the Amount Financed

Seller Financing generally relates to a proportion of the agreed sale price. It is an agreement to pay / fund an amount over time where this principal balance bears interest at an annual rate, i.e. 6% per annum, with the principal and interest paid in monthly instalments based on an agreed period, typically between 1-5 years.

You can calculate the amount financed right now with Flippa’s Seller Financing Calculator here.

Why You Should Consider Seller’s Financing

Whether you are a buyer or a seller, give serious thought to the mutual benefits of vendor financing.

As a seller, if you are in need of the full purchase amount immediately, then of course this arrangement is out of the question. However, you will greatly increase the pool of potential buyers and the purchase price achieved if you are able to offer vendor finance for an agreed proportion of the purchase price. Unlike an Earn-out agreement which is usually limited to a minor proportion of the cost of purchase, does not entail interest payments, and is generally paid out in full within an agreed number of months, seller financing funds a proportion of the purchase with a longer-term payout period and with interest charged on the remaining balance until final settlement.

To illustrate, the owner of the business (owned outright and with no existing mortgages or liens attaching to the business) agrees to a sale price of $100,000. The buyer who has only $40,000 available as deposit, after judiciously retaining sufficient funds for immediate operating expenses and contingencies, has been enticed to pay a premium price because of the availability of seller finance. Ideally, the upfront payment is better to be between 60% and 80% of the total sale value. A reasonable interest rate to be applied to the outstanding monthly balance is agreed in installments preferably no longer than 6 or 12 months.

The interest rate can be fixed, or floating and indexed to the official rate. In reasonable fairness to both parties, because the loan remains essentially unsecured, the rate is initially set commensurately higher than major bank lending rates for business loans.

In the simple illustration above, given the current interest rates and the buyer paying the seller a monthly installment of $1000 plus the applicable monthly interest, the vendor would receive an income stream averaging around $15,000 annually for the five years. The bottom line for a seller who is in a position to defer full settlement is effectively a significantly higher final sale price, while the buyer is able to afford an acquisition which otherwise would have been out of reach.

It goes without saying that a legally binding contract is necessary for this kind of vendor financing arrangement, whereas Earn-out agreements typically rely on a less formal memorandum unless they are particularly complex or involve six or seven figure sums.

Flippa Partner Directory

Find Trusted Financing Partners

Explore Flippa's financing partners who can help structure funding options tailored to your deal goals.

Disadvantages of Seller’s Financing for the Buyer

- Possibility of high interest rates

- Sellers can run a credit check and refuse financing

Disadvantage of Seller’s Financing for the Seller

- There’s more risk involved

- The buyer could stop making payments at any time

- Taxes could complicate things

The Mutual Advantages of Seller’s Financing

While for the buyer the obvious advantage is the capacity to access a business purchase which could not be afforded if the entire amount was required up-front, there is an additional benefit in the continued interest of the seller in the success of the business. Further, the willingness to provide vendor finance confirms the seller’s confidence in the business model and its ongoing viability and profitability.

For the seller, provided access to 100% of the funds from the sale is not required immediately for other purposes, then the regular income stream with an interest rate which is fair and reasonable but actually quite favorable to the seller is a great advantage and effectively raises the actual sale price achieved.

Because the pool of prospective buyers has been increased by the availability of vendor financing, the agreed purchase price is more likely to be at a premium level also. Additionally in some circumstances, there may also be taxation advantages in the delayed payment of the full sale proceeds; this is a complex matter and as a seller you will need professional tax advice on this aspect, but it’s something further to consider.

A Win-win Solution to a Business Purchase Arrangement

While this will not suit all sellers or buyers, seller finance is certainly an option which should be considered. In fact, it’s such a mutually beneficial situation that a rapidly increasing proportion of online business acquisitions are now financed on this way. For most vendors, offering seller finance is a sure-fire way to seal a deal.

Overall 2021 is emerging as a highly promising year for business investment, and we can expect to see exponential growth in seller financing arrangements.

Not Interested in Seller’s Financing and Want Other Options?

You can now get access to finance to purchase an asset via Flippa. Learn more at https://flippa.com/finance.

BUY AN ONLINE BUSINESS TODAY

Whether you’re an aspiring entrepreneur or a seasoned investor, Flippa offers a world class technology platform and advisory team tailored to your business acquisition needs. Flippa has over 6,000 active business listings ranging from $5K to $50M.

Manuela is the PR Manager at Flippa with a love for empowering entrepreneurs to take control of their financial freedom.

Success Stories

Built. Scaled. Exited with Flippa

Hear from business owners and entrepreneurs who have bought and sold online businesses on Flippa.

Calculate your repayments and returns with Flippa’s seller financing tool.

Keep up with the latest from Flippa

Subscribe to our blog and get free tips, advice, and resources delivered directly to your inbox.

Need Help?

We understand that buying or selling a digital business isn’t easy. If you have any questions or require assistance, feel free to contact us anytime.

Contact Customer Support

Search our knowledge base for answers to common questions.