Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

In a transaction that underscores the intensifying appetite for high-margin, niche travel assets, Odyssey Traveller, an Australian-founded stalwart of the educational tourism sector, has been acquired by a United States-based investor for $849,600.

The deal, transacted via the global asset marketplace Flippa, represents a significant exit for a business that has spent 36 years cultivating a monopoly on the “curious senior” demographic. The acquisition signals a sophisticated play into the “silver economy,” where experience-led travel is outperforming traditional leisure segments.

Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

400,000+ Weekly Active Buyers

20+ Multi-language Brokers

Seamlessly Negotiate and Receive Offers

Integrated Legal, Insurance, Finance and Payments

The Asset: A Legacy of Intellectual Arbitrage

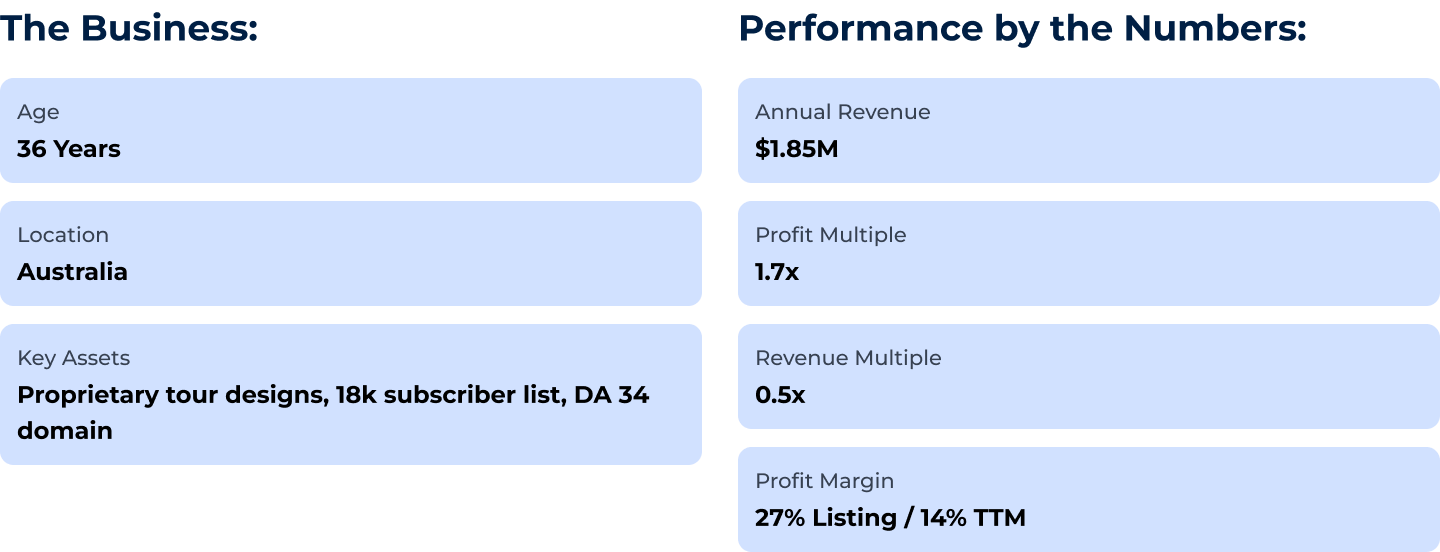

Founded in 1983, Odyssey Traveller carved out a defensible moat by eschewing mass-market tourism in favour of small-group, educational itineraries. Operating approximately 25 to 30 tours annually, the business focuses on “in-depth” experiences, ranging from archaeology to art history, tailored for the 65+ cohort.

The financial profile of the firm at the time of sale was particularly compelling for mid-market private equity and individual investors alike:

- Annual Revenue (TTM): AUD $1,988,314 (approx. USD $1.86M)

- Annual Profit (TTM): AUD $271,795 (approx. USD $496,816)

- EBITDA Margin: 14% (Normalized for industry lean-staffing models)

- Direct-to-Consumer (DTC) Efficiency: 90% of bookings occur directly via the website, bypassing the 10-15% commission leakage typically associated with third-party travel agencies.

The Strategic Rationale: Why the Deal Closed

The $849,600 price tag reflects not just a multiple of earnings, but the value of proprietary intellectual property and digital dominance.

1. High-Value Unit Economics

With an average ticket price of AUD $16,000 per traveller, the business benefits from a premium positioning. The operational model—utilising casual tour leaders and outsourced technical support—allows for a “lean” cost structure that requires only 2 to 4 hours of weekly owner involvement.

2. SEO and Digital Authority

In an era where customer acquisition costs are skyrocketing, Odyssey’s Domain Authority of 34 and its library of high-ranking SEO content provide a sustainable inflow of organic leads. The sale included a high-intent email list of 18,000 subscribers, a critical asset for driving repeat bookings in the senior demographic.

3. Geographic Arbitrage

The buyer, located in the United States, is well-positioned to leverage the existing Australian infrastructure to capture a larger share of the North American market. By acquiring an Australian-based operator with established ground-handler relationships, the buyer gains an immediate foothold in the Asia-Pacific “inbound” sector, which remains a key growth lever.

Transaction Summary

The Outlook: Scaling the “Silver Wanderer”

The experiential travel sector in 2026 is increasingly defined by “purpose-driven” journeys. For the new owners, the growth path is clear: monetizing the existing content library more aggressively and re-launching the inbound tour products for the New Zealand and Australian markets.

As the founder transitions into retirement, the “turn-key” nature of Odyssey Traveller—bolstered by a 2025 infrastructure refresh—serves as a blueprint for successful M&A in the digital-first service economy. For investors, the message is clear: longevity and niche authority are the ultimate hedges against market volatility.

Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

400,000+ Weekly Active Buyers

20+ Multi-language Brokers

Seamlessly Negotiate and Receive Offers

Integrated Legal, Insurance, Finance and Payments

As a Certified Merger and Acquisition Advisor (CM&AA), I help both buy-side and sell-side clients navigate the complex process of selling their online businesses, from valuation to negotiation to closing.

I have over 6 years of sales and online brokerage experience. In my 2+ years working at Flippa I have sold 100+ businesses many as cross border transactions.

You can book a consultation with Fiona to discuss buying or selling online businesses here

Success Stories

Built. Scaled. Exited with Flippa

Hear from business owners and entrepreneurs who have bought and sold online businesses on Flippa.

Calculate your repayments and returns with Flippa’s seller financing tool.

Keep up with the latest from Flippa

Subscribe to our blog and get free tips, advice, and resources delivered directly to your inbox.

Need Help?

We understand that buying or selling a digital business isn’t easy. If you have any questions or require assistance, feel free to contact us anytime.

Contact Customer Support

Search our knowledge base for answers to common questions.