Sell Your Online Business With Flippa

Access expert guidance and the technology you need to list, market and close your deal.

Guidant Financial, the industry leader of innovative small business funding, is teaming up with Flippa, the #1 platform to buy and sell an online business, to speak about the current state of online business, how digital assets stack up as an investment opportunity, and the ways that funding can be achieved in order to become a successful digital acquisition entrepreneur yourself.

Presented by David Nilssen, CEO and CO Founder of Guidant Financial and Blake Hutchison, CEO of Flippa

To learn more about opportunities to fund your online acquisition with Guidant Financial, click here to get started.

Read The Transcript

Benjamin Weiss:

Hey, everybody. Good morning, good afternoon, good evening. Thank you for joining us from all around the globe. My name is Ben. I work here at Flippa. If you were an avid follower of ours, then you likely know me from our daily emails that arrive each morning with some great new business listings. And if you don’t know me yet, well, hello. I’m Ben from Flippa. I’m really excited for our webinar today. For those who’ve been following the stock market today, I know it took a little bit of a nose dive. So I think it’s really exciting that we’re going to talk about some different investment opportunities that might set us all up for a really stellar future. We’re going to be hearing from two different industry greats today. First, we’ll hear from Blake Hutchison, CEO of Flippa about how Flippa’s platform allows you to take control of your future.

And we’ll also get a high level rundown about sort of the state of the digital investment economy as it stands right now. And then following Blake, we’ll hear from David Nilssen, CEO and co-founder of Guidant Financial, who’ll give us a rundown of current business economy out there in the world. And then he will introduce us to some ways that we can value businesses, and of course, how business investment can be funded. To close out the webinar, Blake and David will talk a bit about how Flippa and Guidant can work together to help you guys on your future. And we’ll do our best, as I said, to take some questions from the audience, time permitting. Hope you all are just as excited about this webinar as I am. So without further ado, I will click a few buttons and bring Blake into the video and get things underway. [inaudible 00:01:49]

Benjamin Weiss:

Blake, how are you going?

Blake Hutchison:

Good morning, Ben. Good morning, everyone else. Thanks for joining us today and thank you so much to Guidant Financial and David being with us today. It’s a really interesting session. I’ll obviously take you through a little bit of context around digital real estate and why that’s become such a important and interesting journey for a lot of people. And then as Ben mentioned, David’s going to give you some outstanding insights as to how obviously Guidant works, but also how people are valuing businesses today and ultimately how you can use alternative ways to acquire capital or access capital for the purposes of acquiring a business.

Flippa – Blake Hutchison

Blake Hutchison:

Thank you very much. So one of the really interesting things that is right now is this insatiable demand for not only the digital economy, but what we call digital real estate. And that’s simply because the world is transforming before our eyes. There are more people online than ever before. There are more people consuming content. There are more people consuming e-commerce. And as a result, we have this huge growth period through all of the different platforms that power the digital economy, be it Shopify for e-commerce, WordPress for content websites, Amazon, where you want to use Amazon’s powerhouse distribution opportunities. So it really is such an exciting time. And so I just wanted to point out a couple of things. What is happening on Flippa is we are seeing more than ever before, buyers want to jump into what we call the digital real estate market. And digital real estate, no different to tangible real estate, property.

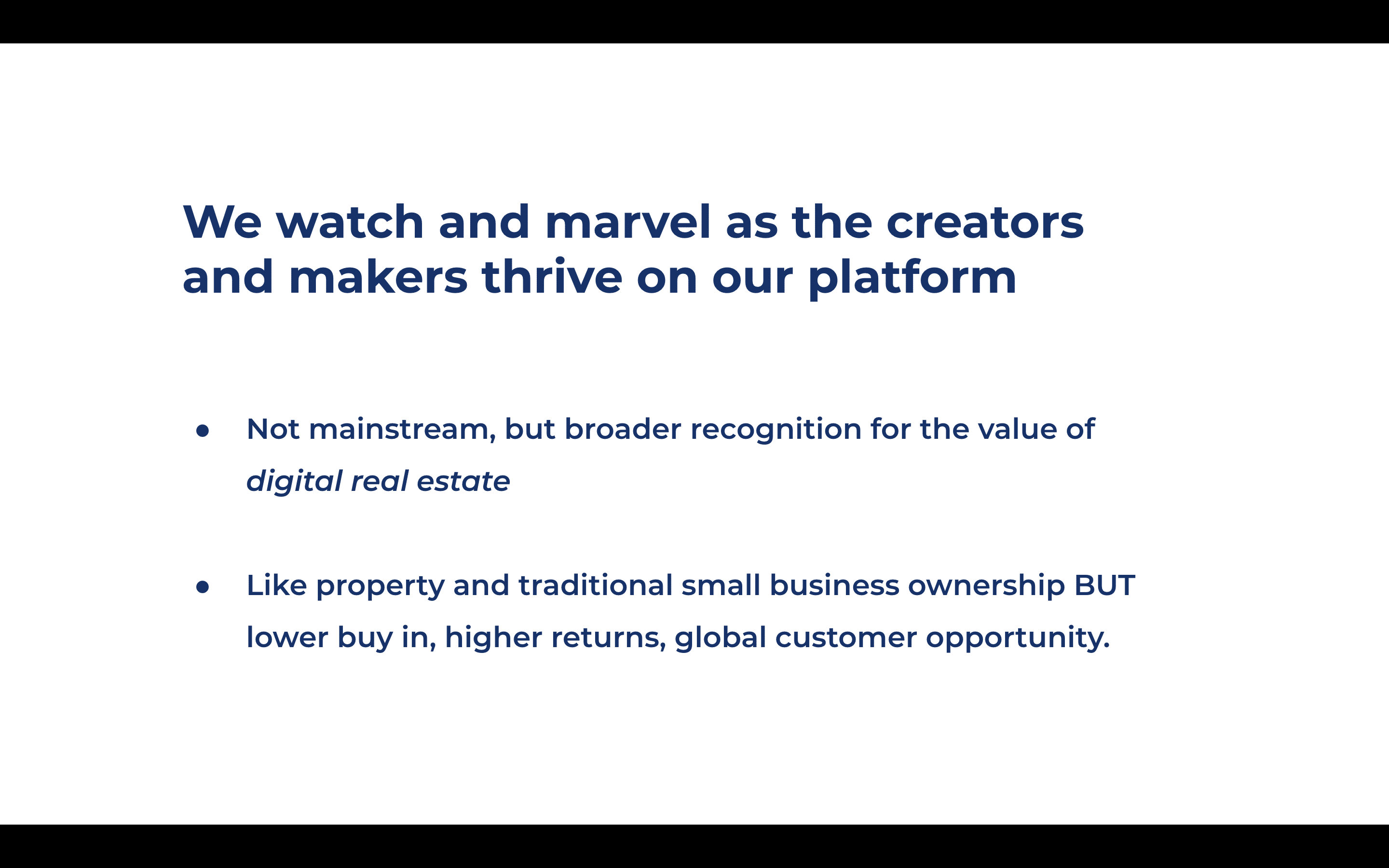

The difference is now there’s a broader recognition for the value of digital real estate. People are really starting to understand that this is a viable asset class. It’s an asset class which will, typically for most people, require a lower buy-in. So you won’t have to spend it or invest as much to get in, in the first place. As we’ll point out in a couple of slides, with digital real estate, you can also typically get higher returns. And that’s because right now the valuations for digital real estate aren’t as great as they offer other asset types. And then of course, as we see more than ever before today, there’s a global customer opportunity. So for us here at Flippa, it’s super exciting because what we watch play out on our platform each day on the number one marketplace to buy and sell digital real estate, what we see are creators and makers.

So those people who are small business owners, but in the digital ecosystem predominantly meeting buyers who are looking to get into the digital economy for the first time, or are looking to continue their investment trajectory in this particular space. So it’s quite an exciting time. And I suppose the question that we like to ask now of all of our customers is, given how much transformation there is worldwide, will this be a transformational time for you? There’s a lot of people entering the digital economy for the very first time.

And why? Why Is it so exciting? Well this seems obvious, but I was absolutely staggered when the McKinsey Consumer Sentiment Survey of June, 2020 came out to say that 40 to 70% growth in consumers who purchased most or all of their items online for almost every category. Now, I don’t know about you, but I’ve met people who, before this COVID-19 period, were less familiar with e-commerce, were less comfortable with technology in general. And that has changed dramatically. It’s changed so dramatically that 40 to 70% of customers in North America now purchase most or all of their items online for almost every category. And so this transformational shift is impacting us all. And ultimately it means that if you are considering investment in digital real estate, this is probably the time to do it.

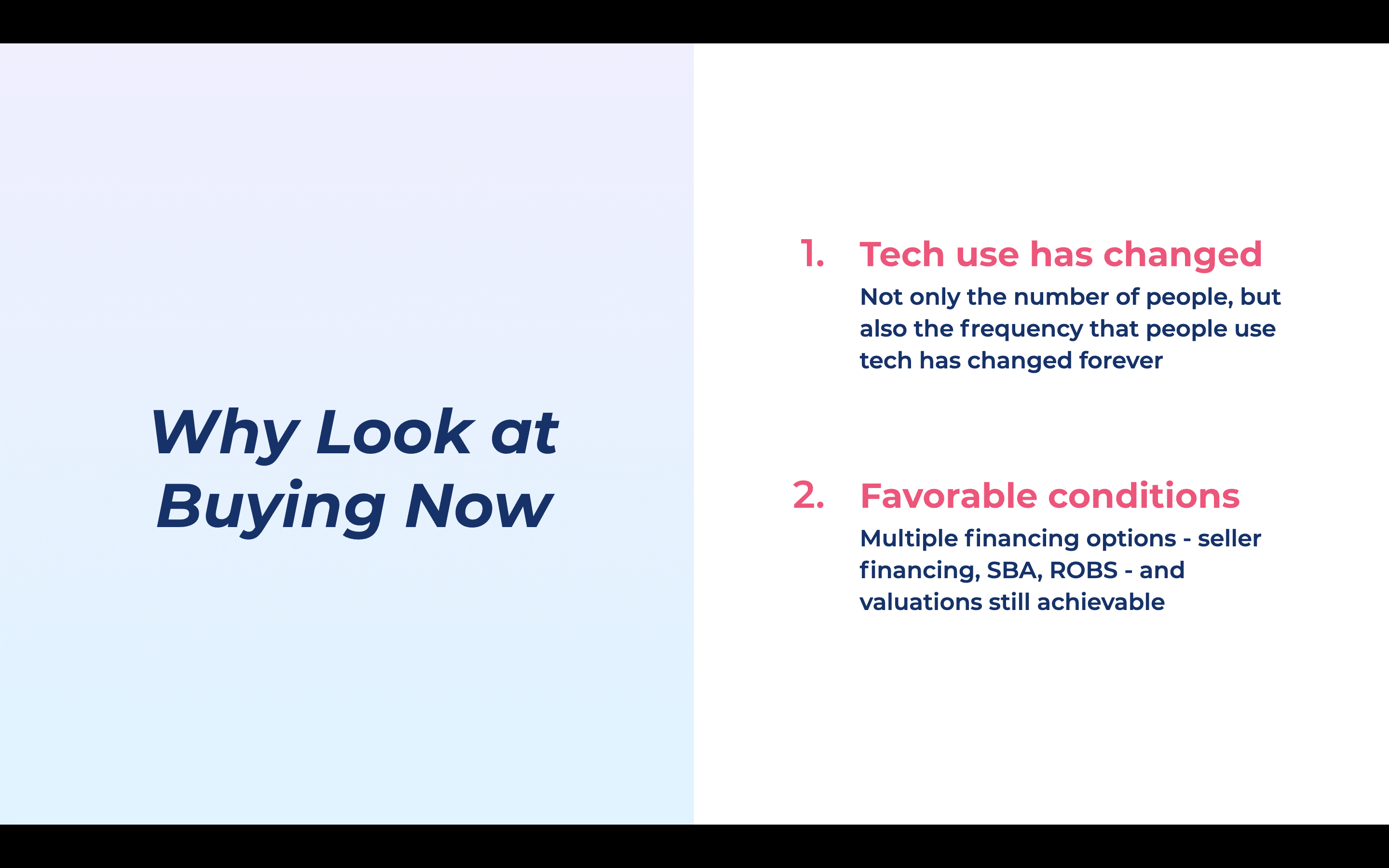

So if you’re in the market to buy something, let’s just roll up the reasons why. So one, we talked about this tech use has changed forever. The number of people using technology to drive their day to day purchase decisions, their day to day research has changed forever. It’s not only that more people are using tech, it’s also that the frequency that they use it has increased so dramatically. But more than that, and David will speak to this a little bit, there are favorable conditions for those people who are looking to buy now. And so we see two types of buyer. There’s the buyer who is looking to acquire digital real estate to supplement their income. So they’re like you or I. They work in the corporate sector, maybe they work in the traditional small business environment. They’re looking to supplement that income through the purchase of digital real estate, or they are investors, they look to acquire multiple assets and aggregate those assets for the purposes of driving greater value longterm.

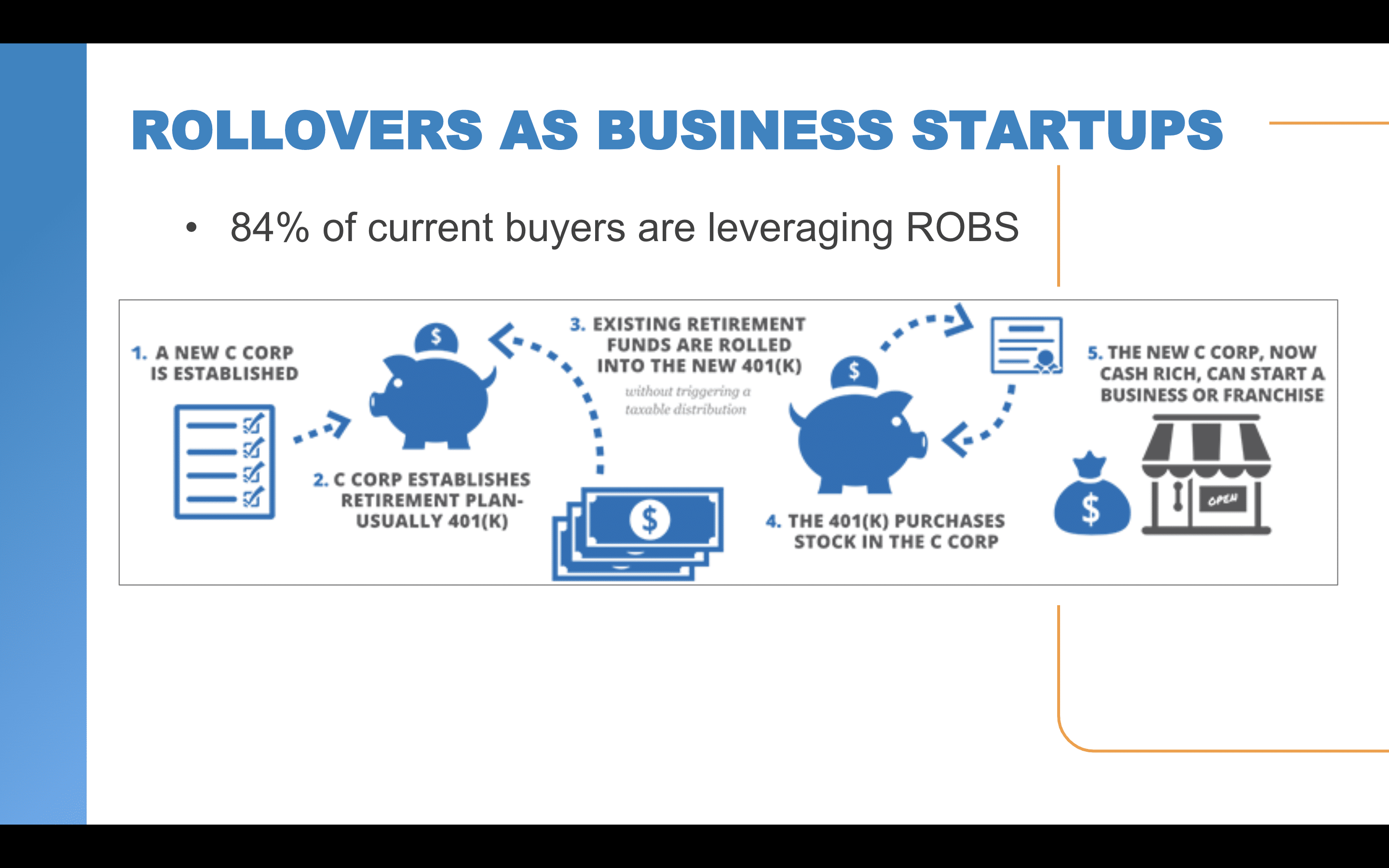

And so the conditions for these individuals are more favorable than ever before. There are multiple financing options and David will talk to this. So there’s seller financing, which is where you don’t necessarily use a financial services or financial institution to back your acquisition. You’re more working with the seller and they are financing the purchase and you’re paying down the loan to that seller. There’s SBA, so small business administration loans. ROBS, which David will no doubt speak to, a rollover for business financing using your 401(k). And it’s also very favorable right now because valuations of digital real estate are still achievable.

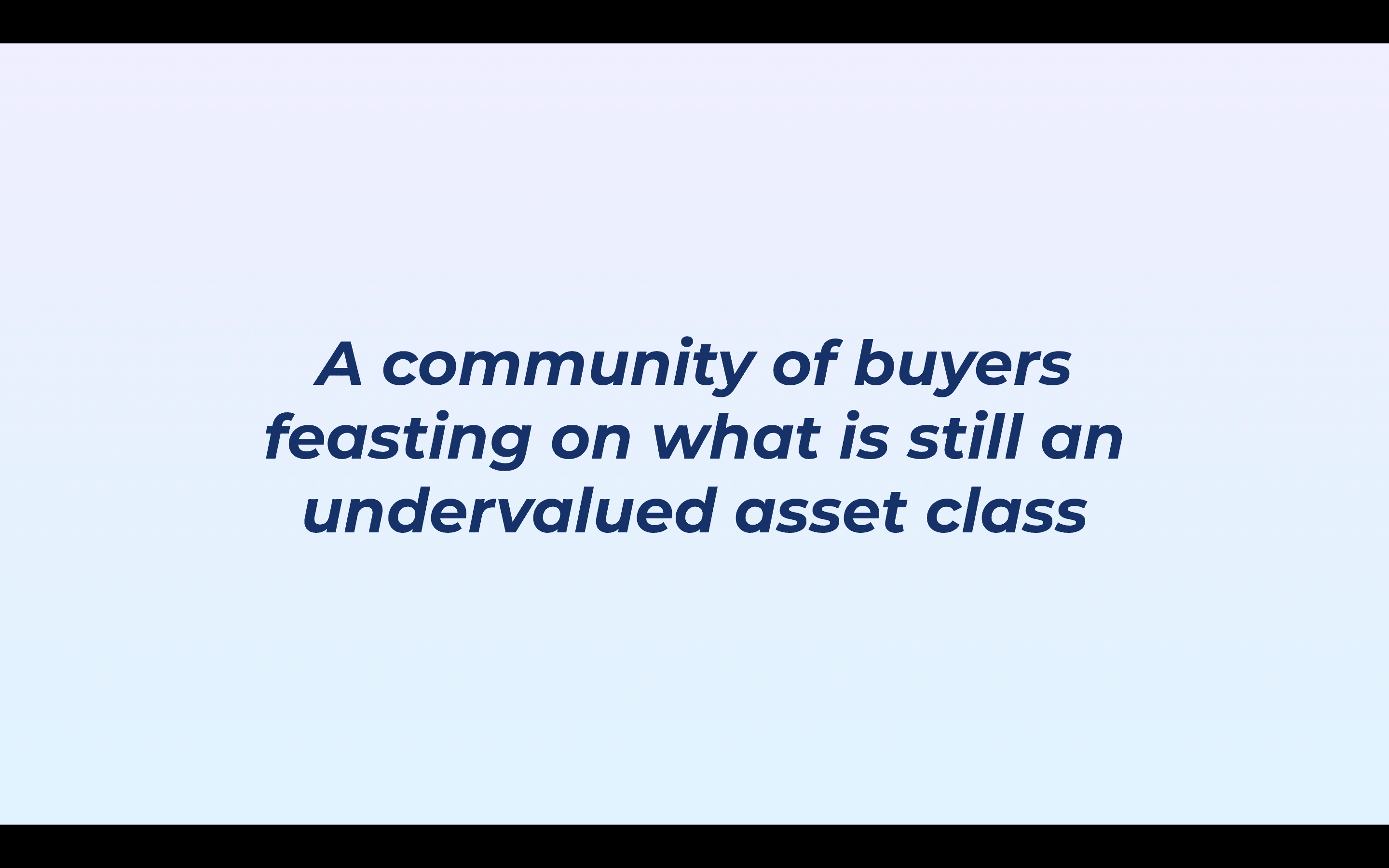

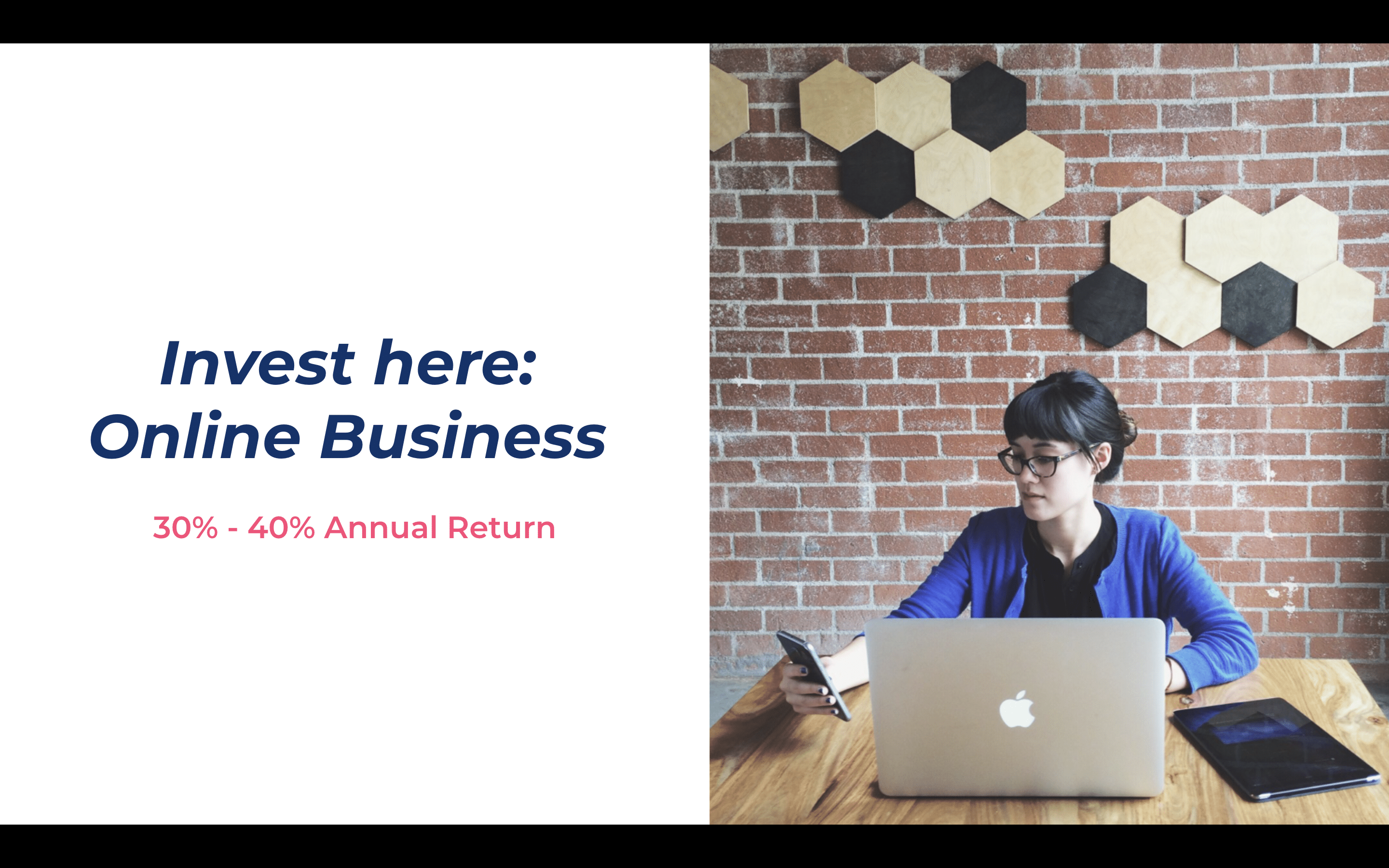

So we talked about this, a community of buyers feasting on what is still an undervalued asset class. So more exciting than ever before, but let’s take a very, very simple view of the world. So you can invest here in real estate. It looks like a lovely home and perhaps get a five to 7% annual return if you’re lucky, depending on the market that you are operating in, of course.

Now this is having a good time of it, the S&P 500. So typically you’ll derive an annual return of seven to 8%. And of course, as I said, it’s having a good time of it. So as a close of trade on Tuesday, the S&P was up 9%. So that’s pretty exciting, but is it as exciting as this? So you’re buying is lower.

Valuations are far less than you might get through a business traded on the stock market and your returns are substantially greater, 30 to 40% annual returns. So let’s just ram that home. Let’s say I have $15,000 to spend. Let’s say I’ve got an asset which is earning $500 per month, $6,000 per annum. I paid just over two times net profit to acquire that asset for the $15,000 that I’ve got to spend and I’m getting a 40% annual return, so long as that asset continues to perform at the same level it did prior to my purchase. That sounds like a more sensible play to me. Don’t invest in a car, check out real estate, check out the S&P 500. Now compare that to online business, 30 to 40% annual return. Sounds like a good pathway to me.

So there’s never been a better time. Hope you all take the opportunity to own your future. The more exciting part of this talk begins now with David and his awesome insights. Thanks, Ben.

Benjamin Weiss:

Fantastic. Great stuff, Blake. David, who we’ve talked about a few times already is CEO and co-founder of Guidant Financial, a fantastic company that it’s obviously been quite critical in helping entrepreneurs realizing their dreams of owning small business. So David, I’m going to get your video started here.

Guidant Financial – David Nilssen

Great. Well, I appreciate getting a chance to be on here today with you. It was nice to hear Blake’s thoughts about the online market opportunities. And I am eventually going to go into covering financing and how to think about valuations in this environment, but I do want to share a little data to frame the conversation specifically around COVID-19, because we are still in a pandemic and it is having an impact on all of these things today. Now, I’ll fully admit that Guidant Financial works with new entrepreneurs as they think about either buying or starting a business, but we are limited to the domestic borders. So you’ll see that a good portion of the data is related to the US and while we’re talking about different industries, I also am going to pull in some information around brick and mortar, small businesses, mainstream American small businesses. And my hope is that it will either expose or at least help to provide some thinking around where there may be opportunities and even online. So let’s go ahead and just jump straight in.

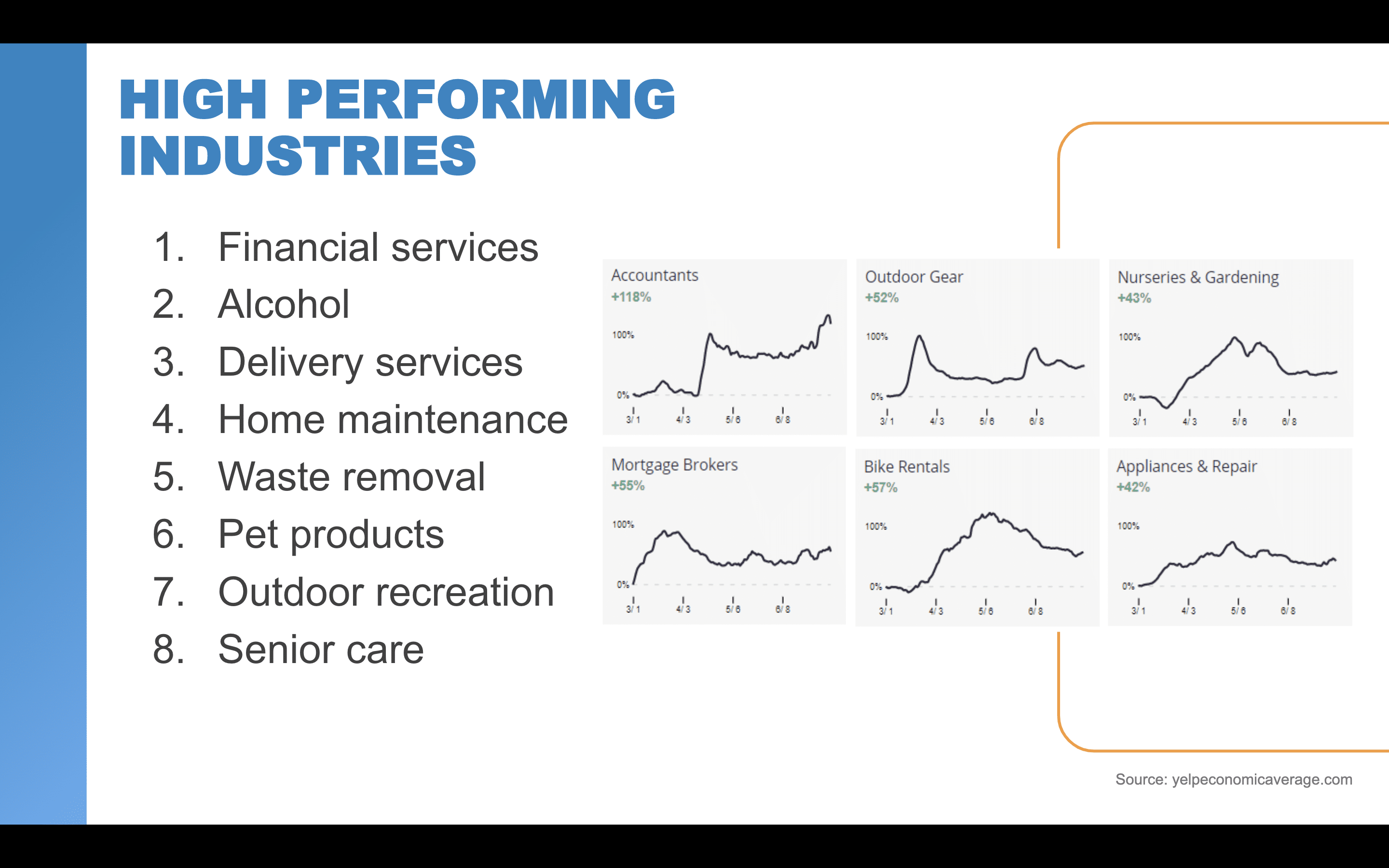

So there are many thriving businesses in this environment and industries or categories that have demonstrated that they’re not only recession resistant, but in some cases, a crisis can actually be an accelerant in those models. It’s not surprising that financial services and insurance attacks are performing well. And given that we’re in a low interest rate environment, mortgage is also on the rise, but there’s some other categories that I think are at least worth understanding, because if you looking at an online business, these may be categories that you want to be aligned with in one way, shape or form. So I’ll talk about alcohol. We’ve helped to fund businesses in the US like Dry Fly and NoDa Brewery, helped them obtain funding, but these types of businesses can see increased demand. At one point, Yelp was suggesting that the searches for wineries and breweries was up over 100% as people were getting ready to hunker down at these stay at home orders. And I’ll fully admit, I might have been part of that statistic.

But delivery services have shown to be imperative for groceries and restaurants and businesses that want to continue operating in a time when people can’t. Blake talked about this a few minutes ago, but there are lots of people, including my parents who had never used Amazon for delivery services, and now may not ever go back and I think it’s likely to be the… Consumer behavior has fundamentally changed, giving an advantage to digital properties longterm. Package ship locations are doing really well right now. They’re helping to transport goods directly from those businesses to people while they’ve been shut down. And I personally have been to the local UPS store franchisees’ location no less than 10 times since we’ve been experiencing this event, but those delivery services, if someone can deliver these types of services quickly outside of having a physical location and they certainly have an advantage.

And another category that’s really interesting is that, people being home, we’ve seen a rise in home projects, gardening and even repairs. In fact, I was speaking to my brother who shared that in the past four months, they have replaced their roof, redone their insulation, re-landscaped their yard, re-paved their driveway, and now are contemplating some additional projects. So the home improvement category, especially online, is seeing some significantly increased demand.

The last thing is just pet care, pet products, pet adoption. We’ve seen 50% growth in pet adoption since COVID took place. In New York, it’s 10X the norm, 70% higher in Los Angeles. So this has created demand for those mobile pet products, mobile pet… Pet care, excuse me, and something certainly worth noting. And then the last thing I’ll just note is that senior care, senior services, senior products are certainly thriving, and this has been effectively, or excuse me, essential in the pandemic because many families have had limited access to each other and because of that they’ve had to increase care through other means. So that is something certainly worth looking at.

And I’m sure there’s others out there, but these were some of the industries that we see that are doing really well. And if online businesses are serving these groups, then they should be seeing some great momentum as well. Now, I do want to talk about the darker side of the pandemic. Blake talked a little bit about the innovation that has been occurring, and I just want to share that I’ve been also really impressed with the amount of innovation that the entrepreneurs have been showing. Franchise systems like Clean Juice quickly pivoted from being made to order, to grab and go. I know baby products here in Seattle, Washington, where I’m at that shifted from making baby products to immediately doing decorative masks for children.

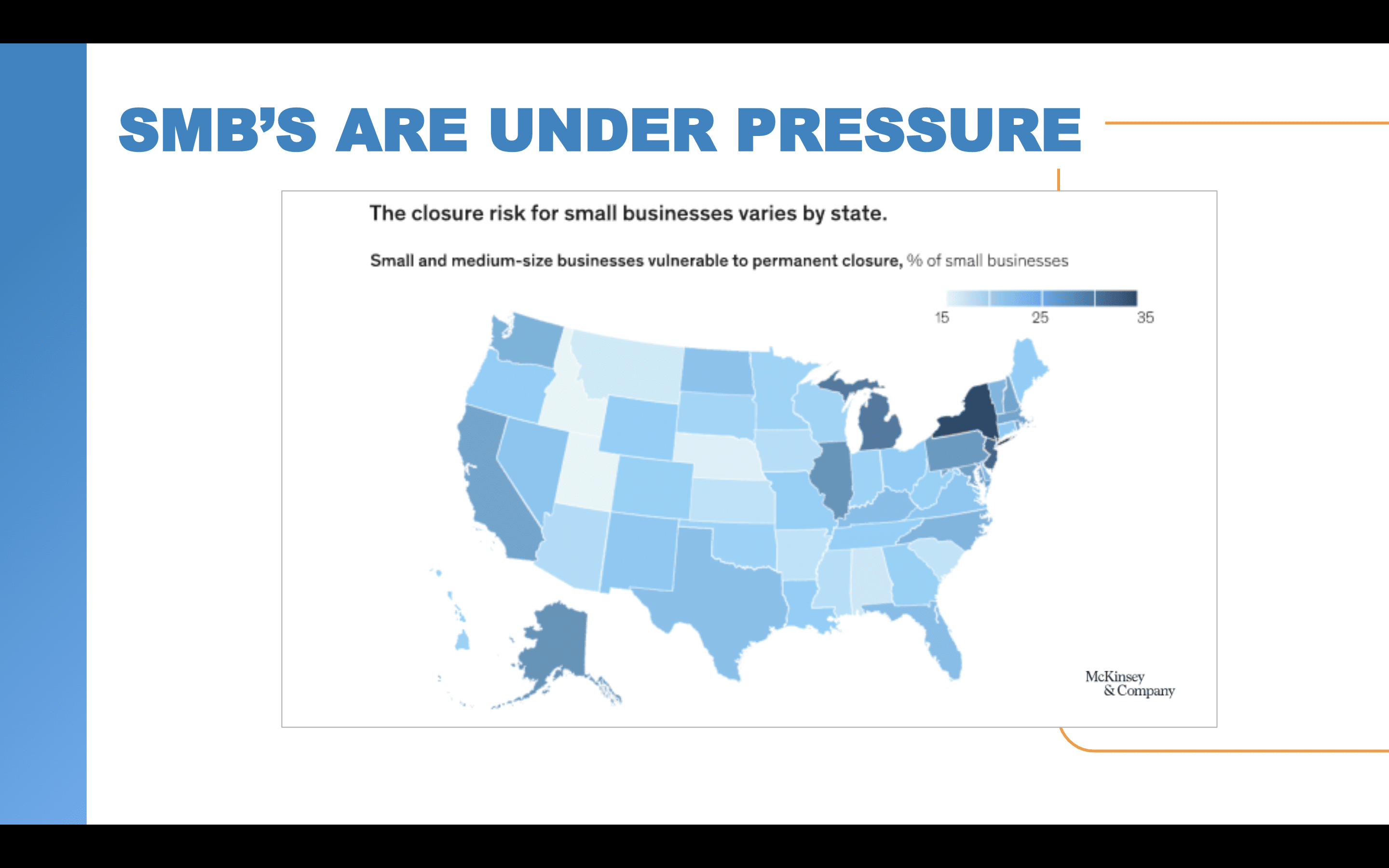

And then there was a Seattle entrepreneur here that had a restaurant. They knew that they had to create something different because of the socially distant experiences. So they turned their parking lot into a beach, brought in a boatload of sand and started doing dinners and movies in a socially distant manner. But even though there’s lots of great stories, there’s still so many businesses all over the US that are under significant pressure. And the harsh reality is that hundreds of thousands of them will not survive.

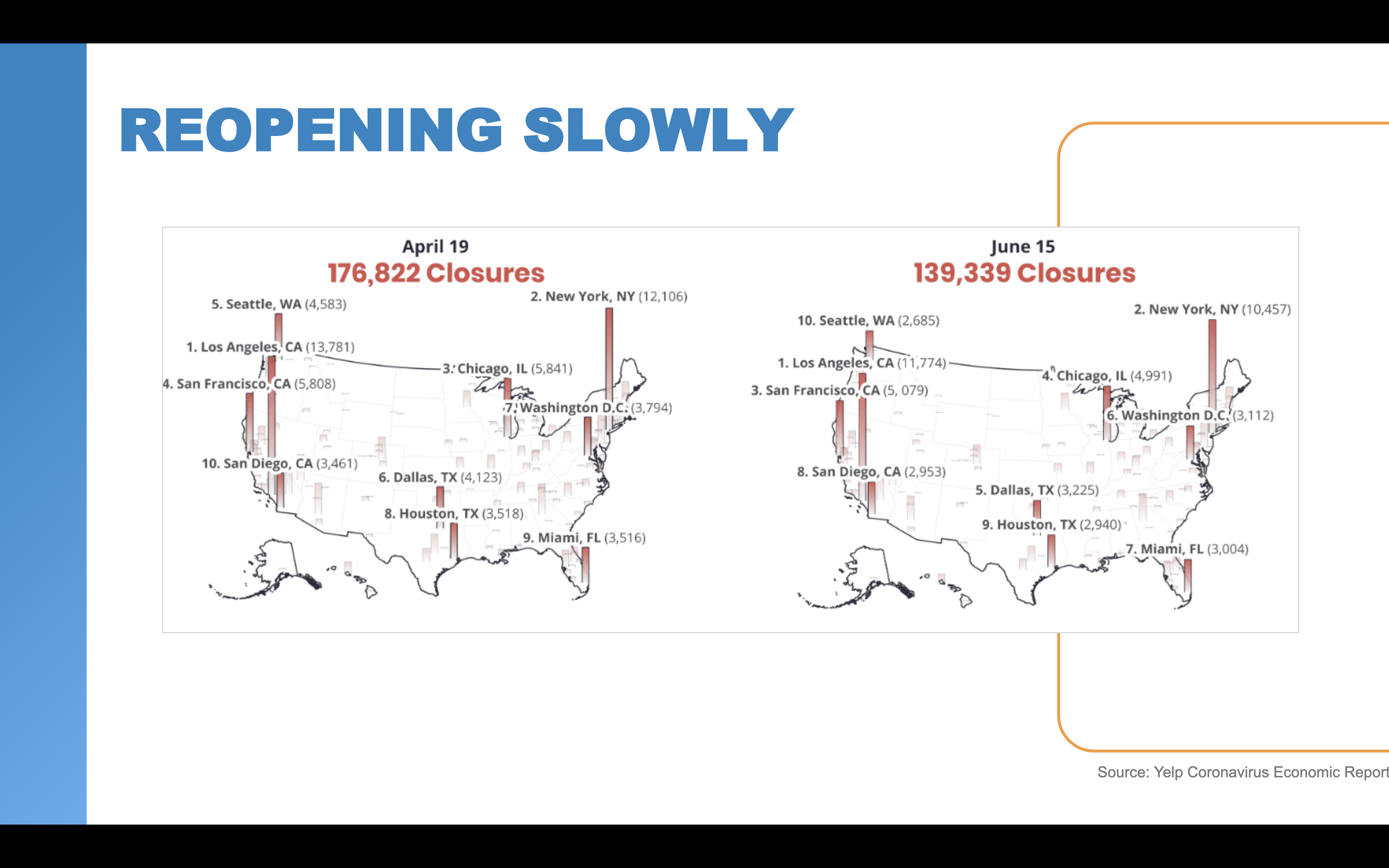

In fact, Harvard estimates that about 100,000 of those small businesses have already gone away. Now, the graph that you’re seeing here comes from a report by McKinsey, where they suggest that between 10 and 35% of the small businesses, depending on their geography, are at risk. So that is obviously troubling, but the need for those products and services aren’t going to go away. They’re going to shift to other places like online.

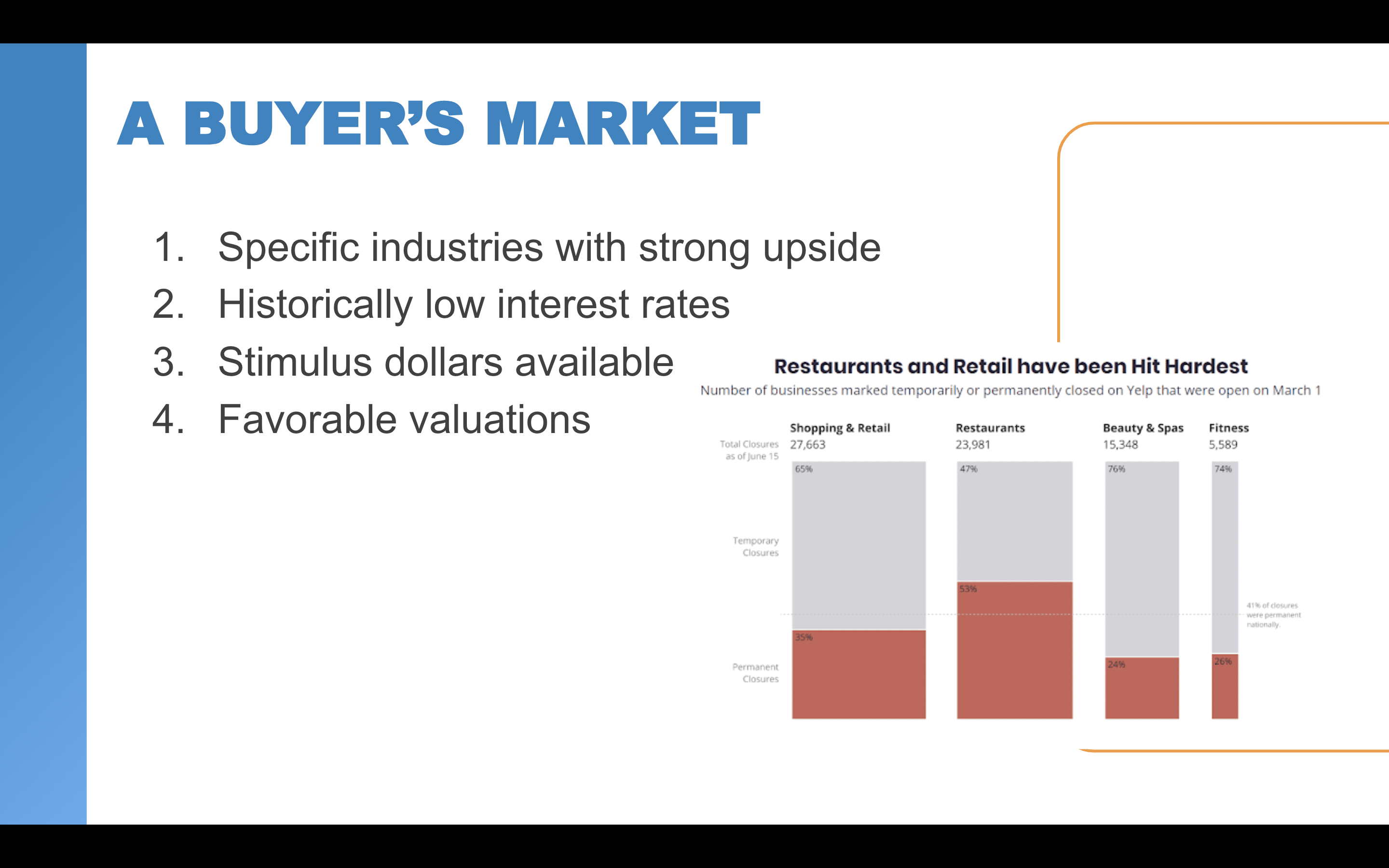

So those industries that are under pressure also potentially create lots of opportunity. Now, Blake talked a little bit about this right before he closed and that is we see this as a buyer’s market. There’s many businesses who have increased as a result of the pandemic, and they can be really strong, stable, and predictable opportunities, both online and offline. But, we all know that businesses who rely on foot traffic had been undoubtedly hit the hardest. And so today, Americans are saving at a greater rate than ever before, and they’re not spending as quickly, which is also impacting some online properties. So for those of you that have a bit more risk tolerance, there’s a great opportunity to, for buyers, I should say, to acquire businesses that have really great upside potential. Now I am not advocating that anyone take advantage of someone who’s in a struggling situation.

Certainly never liked to see anyone fail, but, small business failures can be a catastrophic financial event. So if someone who might close otherwise can transfer that business or those obligations and walk away with a little money in their pocket, it could be a meaningful, positive experience. So, just a couple of things to think about, some industries that we believe are really gaining momentum right now. One is cleaning and sanitation supplies. A good example of this, I have a friend that owns a commercial cleaning business, and right now, for things like masks and other imperative personal protection equipment, they are being required to order significantly larger amounts of inventory and there’s an opportunity for aggregating those products into one company and selling them off in batches. So I think cleaning and sanitation is going to be something that’s really important because it’s in high demand right now. And for the smaller businesses, they’re going to have a hard time getting a hold of those.

Now, it’s also important, because as businesses are trying to open under new standards and schools are starting to reopen, that’s going to create additional opportunity. I suspect this is going to be an exciting space for quite some time. Tutoring and e-learning also has massive potential because of the challenges with reopening schools and the potential for shutdown. So something worth looking at, and then home video health and fitness concepts are going to continue to be popular. In fact, Taboola reported that there was a two million percent increase in article traffic around that topic specifically. And today, I’m not sure how many people are running into gyms where they’re perspiring amongst lots of other people. So who knows how long that will last, but I believe that that’s a trend that’s here to stay.

Regardless of what you choose, the question is, how do you determine the price or fair market value? Now, technically if you and a seller agree on a price and they’re not under any duress and your financing can support it, then that’s sufficient. However, I certainly would recommend getting a certified appraisal when making a big investment and big is a relative number and only you can determine what that is. But we complete thousands of business appraisals and valuation reports every single year and there’s often a gap between the initial price or estimated price upfront and then the final determined value. And online businesses are a bit trickier because they’re usually a niche and sometimes it’s tough to find comparables and they don’t often have a lot of tangible asset value. So in order for the appraiser to do their job, they have to get a deep understanding of the business.

And as a result, you get insights into where the value is and where you can grow. You understand the areas that they might discount because of risk and things that you can mitigate against. So it can be really helpful, particularly because they’re so nuanced. So for example, retail e-commerce is going to be perceived as a riskier than wholesale e-commerce or B2B. Not all income is the same. If it’s recurring income or products that support a higher lifetime value and create repeat business, then that will always be valued greater than transactional cash. So lots of interesting scenarios will play out today and in this environment, so it’s probably more important than ever that you work with your CPA, maybe a broker, if you’re working with one and then the financing company to hone in the right number.

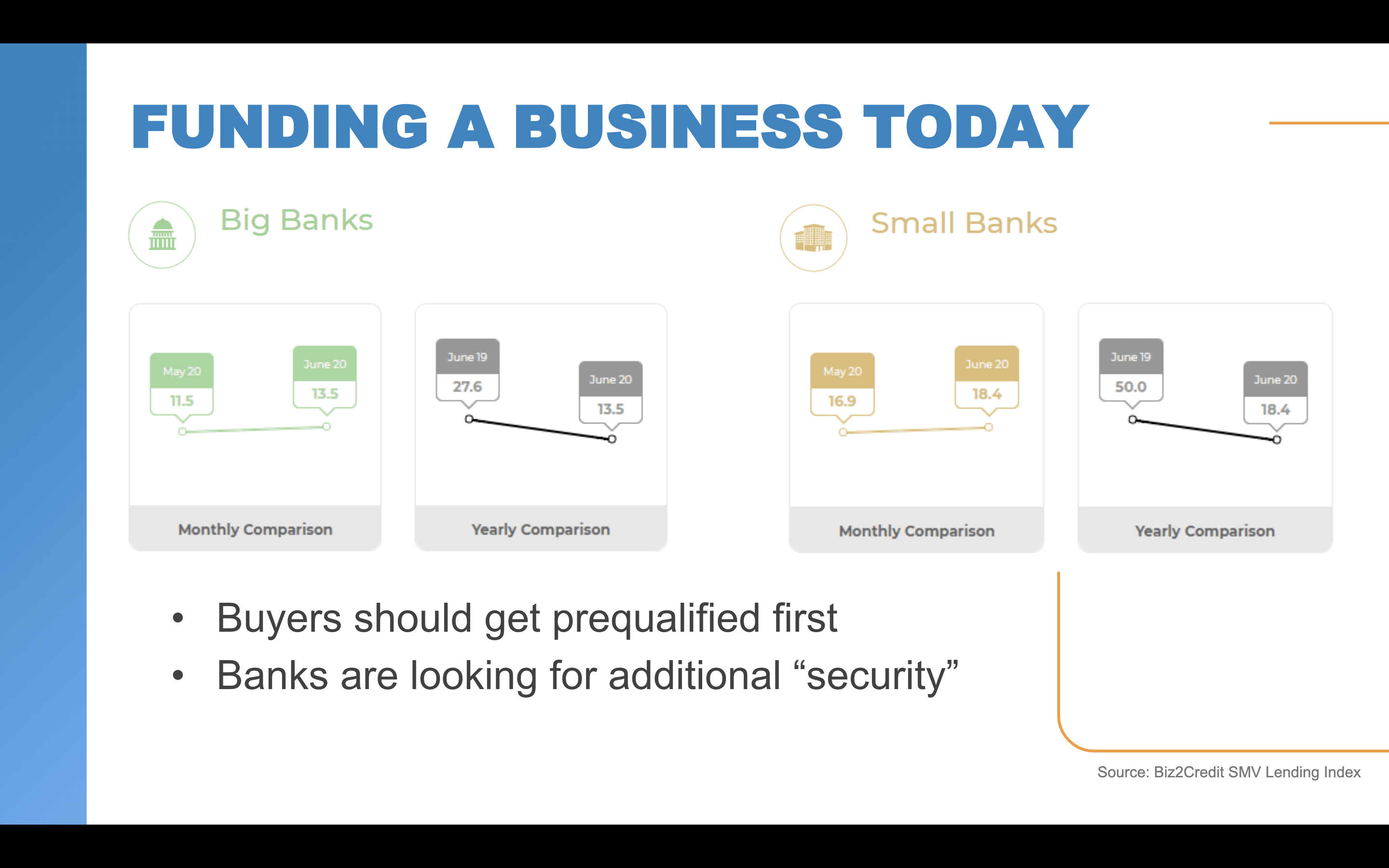

So let’s talk then about financing. Oh, you know what? Actually one other point that I want to make about the value. One thing that you’ll want to be clear on is if you’re buying in this environment today and the business is in an uptrend, you may want understand how much of that is just based on the normal business, the course of growth, some changes that they’ve made and what might be being propped up because of the pandemic. And you certainly will want to make sure that you understand that because as things start to return to normal, whatever normal means, you may want to consider what the impacts may be to that business. Now, in terms of bank financing, we work with buyers every single day to pre-qualify them, to build a strong financial package and then to locate the right bank and where possible help to appropriately address the conditions that occur going back and forth.

But I will say that the lending environment is hard today. You certainly don’t want to passively address financing. Small business lending has dropped off significantly and while it’s slowly making its way back, it is definitely a ways off from where it was in 2019. And as you can see on this graph, the banks, the big banks are approving only about half as many applications as they were last year and small banks have dropped off by two thirds. Now [inaudible 00:22:31] really a big surprise in the past four to five months, the banks have been distracted by the Paycheck Protection Program and trying to get dollars in the hands of their current portfolio, but it is starting to pick back up. And one thing I’ll note is that in times of uncertainty, banks will tighten up their lending practices. So while lending is available and we’re seeing the demand for loan applications is increasing month over month, it is a challenging environment.

That being said, it is a great environment for qualified borrowers because of the economic conditions. Today, we are enjoying historically low interest rates. So SBA loans are being provided at five and a half to 6% over 10 years, and sometimes at fixed rates, but the banks are underwriting at a slower pace, especially with online businesses where they’re going to place emphasis on certain areas. So if you’re looking at online property, just a couple of things to note, if you’re going to use SBA financing, they’re likely to require a 700 plus credit score, they’re going to want to see that the business plan itself accounts for COVID and it has a believable strategy. They’re going to want to see that there’s relevant experience. This is particularly important for retail businesses like restaurants and fitness and hospitals. They want to see someone’s got that relevant experience, but with online businesses, if you’re a yoga instructor and you’re looking to buy an online yoga studio, that is not likely to be considered relevant. We’ll want to see somebody who had a little more experience operating digital properties.

And then finally, the look at capital coming in. The banks are likely to suggest at least 20% down. Again, if you’re looking at SBA financing, but for strong borrowers, if you’re well prepared and you have a great financial package and relevant experience, you can get really favorable funding. If you haven’t already, though, I do recommend getting pre-qualified. It takes very little time, but it can save you a tremendous amount of it when it becomes important.

Now that was about SBA lending, but there are lots of options outside of the banks, many of which allow you to make the sole decision in terms of whether or not you get funding versus where the SBA, it’s really up to the underwriters. Now, if you’re buying a business and need less than a couple hundred thousand dollars, there are some options out there like unsecured credit, which is more akin to revolving credit, such as credit cards. Home equity is dirt cheap and then ROBS, rollover for business startups.

Now, Blake briefly introduced this, but I’ll talk about it in a second. I just want to make a note that there are risks in any business investment and how you finance it has pros and cons. But for today, about 90% of the transactions that we see are rollovers for business startups arrangements, we’ll do a couple thousand of those annually. This is a little bit newer concept for most people, so let me just explain what it is. ROBS allows an individual to invest up to 100% of their retirement assets into a small business without taking a taxable distribution or getting a loan. So to illustrate this example, I’m going to use Microsoft. You can buy stock in Microsoft inside your 401(k) plan, and at a very high level you’re sending your money to Microsoft. They get to use those dollars to grow their empire, and you get to hold shares in the business’ collateral per se, for making investment. And if you do well, your investment grows in value and if you sell it, the gain goes back into your retirement plan where it’s either tax deferred or tax free.

The same thing is happening here through a rollover for business startup or ROBS plan. You are making an investment into a privately held enterprise where your retirement plan becomes a shareholder because of it. It’s an investment, so it doesn’t trigger a taxable event and it’s not a loan, so there’s no payments. And this means that the business, as it generates income, can reinvest back in the business rather than sending those dollars off to a bank in the form of interest payments. And the funding’s fast, it can happen in about three weeks or so.

Since the pandemic started, the stock market has certainly done well and as Blake talked about, although today was a tough day, I think actually Ben might’ve made the comment. Today was a tough day. In general, it is back to its pre-COVID levels. And so many of our are choosing to sell now and redirect those funds into something they have more direct control over and where they think that it will outperform the stock market over a period of time.

Okay. I know I’ve covered a lot in a very short period of time and I’m sure there’s questions, so I’m going to stop here, give control of the screen back to the team and maybe we’ll jump into some Q and A.

Questions & Answers

Benjamin Weiss:

Yeah. Fantastic. Man, that was fascinating stuff. Thank you for that, David. I’m learning a lot about financing from you today like everyone else. I appreciate it. Blake, and I was curious, I know we talk about valuation all the time at Flippa. Curious what your thoughts were on some of David’s comments kind of starting back there.

Blake Hutchison:

Yeah. Thanks Ben and thank you, David. Super insightful. Really, really appreciate that detail. Look, Ben. One one of the things that I am completely aligned with is David made the statement that there is often a gap between the initial valuation and the sell price and that’s by nature of buyers… Well, it’s either a very much in demand asset, in which case there’s buyer competition and therefore valuations are pushed up, or it is that you’re dealing with a niche and there’s a specific buyer who’s interested in that niche and that’s not something that could have been taken into consideration through a formal valuation, but that is something that we encourage all of our sellers to be aware of.

Blake Hutchison:

We often see on Flippa that people will use the valuation and they will consider it such a strict measure of their business that they’re unwilling to entertain other ideas of valuation. And ultimately fair market value is what a buyer is willing to pay. And so what people will find is that it could be slightly less than the formal valuation they’ve received from somebody, or it could be slightly higher. And it often depends on how much appetite there is for the buying community. In e-commerce right now, across things like toys, across things like fitness, valuations are being pushed up far in excess of what a formal valuation might expose. And so clearly market timing and circumstances come into consideration too.

Benjamin Weiss:

Yeah. Super interesting stuff. There’s a couple questions coming in here, Blake, I saw on the side and David. Actually, they seem to be more presented at David. Some investment questions. Well, let’s see. Beverly just shot one through really quickly. She’s curious, are banks willing to do a combination of a down payment and seller financing? For example, say a buyer has 10%, seller willing to do 10%. Will banks accept this combination for a required 20% down? David, you want to take that?

David Nilssen:

Yeah. Great question. The answer is they can. Yeah, I think there’s a lot of different ways that people can bring liquidity to the table. At the end of the day, the bank is going to want to know… Some of the things that I talked about, it’s a believable business plan. They see that the financing can be supported by the business itself, but I think in short, the answer is yes. Ultimately it’s going to come down to the business itself. I will make a quick comment about something Blake said just a second ago. I want to make sure that I was clear in the presentation because I don’t want to send the perspective that a certified appraisal is the end all number.

David Nilssen:

It is important when you are using bank financing, because unfortunately the banking system is a little bit behind and they just have a hard time wrapping their brain around online business valuations. And sometimes there are strategic value adds inside of an online purchase that you just can’t get from income or assets and the comparables may not be available. So ultimately, he’s absolutely right in that fair market value is determined by the buyer and the seller. It just needs to be supported by the financing.

Blake Hutchison:

David, I might ask you a question just on the rollover for business startups. We see that coming up a little bit, but perhaps not as much as we might’ve expected. I think you mentioned that 20% of all Guidant Financial funding right now is in the rollover for business startups, sector, or product type. Are most people using that to acquire an asset or business, or are they using it for growth capital?

David Nilssen:

Yeah. Great question. So strategically, our business is focused on helping people at the point of acquisition. So it’s when they’re actually going into business at first. Working capital, if you’ve got a good business and you’ve been the operator for some time, working capital isn’t so hard to get your hands on. But from the very beginning, it can be very challenging, even for very financially qualified individuals. In fact, I didn’t put it in here, but what we see is that about eight out of 10 people who go to a bank, and this is including those that already operate a business, are going to get declined.

David Nilssen:

So even strong borrowers who operate their own business have a very low likelihood of getting funded successfully. But for us, we are focused on helping people as they are first going into business for themselves. Now, this statistic I cited actually is, in the pandemic, it’s been about 90% of our business has been in rollovers for business startups. That’s proportionally a little higher than normal. That’s partially because the banks have been a little bit apprehensive to lend in this environment. That’s getting better, but it has been more difficult in the past six months.

Blake Hutchison:

Okay. And if you don’t mind a quick follow up question there, what percentage of a 401(k) are people typically rolling over?

David Nilssen:

Yeah, it’s been a while since I’ve seen that statistics. So I want to be careful not to quote the wrong one, but the last statistic I saw is about 60% of people that were rolling their assets were rolling over 75% of it. So people were making a significant investment, if you look at it as a proportion of their actual savings, but I think that shouldn’t be terribly surprising for anyone who’s entrepreneurial minded because these people are choosing to go into business for themselves because they believe in their ability to lead and guide this organization, and they believe the model is a catalyst to higher returns, as you pointed out earlier there. So not surprising to see that’s the case, but that was the last statistic I saw, but it’s been over a year since I looked at that.

Benjamin Weiss:

[inaudible 00:33:32]. There’s actually a question from the audience that might make a nice follow up on that too. Christopher’s asking when you do invest with a ROBS, can the investor take an income out of that or does all the revenue go back into the 401(k), he’s asking?

David Nilssen:

Yeah. Great question. And I suspect that the question is coming because they’re familiar with the self-directed IRA industry, which is a sister product or industry, but it is not directly on point. So there are explicit exemptions in the tax laws that allow for investment into small business. This was intentionally put in place by Congress to encourage investment in small business. And it does allow the individual, as long as they are paying themselves a reasonable salary, one that is like what any entrepreneur in that industry and in that area for a like business would pay themselves, then they are allowed to pay themselves a business and take an income from it at the same time as their retirement plan, as a shareholder. But under IRA law, that would not be possible. So Blake pointed this out and I actually glazed over this. This is a 401(k), so this is taking any sort of retirement assets that you have, whether it’s in an IRA or 401(k) and rolling that into a qualified plan or a 401(k) to make the investment.

Benjamin Weiss:

Interesting. [crosstalk 00:34:51]. Go for it.

David Nilssen:

I have a question for Blake though, because, Blake, you were talking a little bit about consumer behavior and I threw in the anecdote there that my parents are now online shoppers. I’m just curious from what you guys see at Flippa, what type of businesses are moving right now? Where’s the greatest interest? And do you think the consumer demand has changed forever?

Blake Hutchison:

Great question. My personal opinion on this, and I hope there’s not too many people that get offended or dissuaded by this comment, but my personal opinion is that we are not going back to normal and that our lives and the way we undertake business has absolutely changed for ever. And so that there is going to be more and more opportunity in the digital economy. And I’m not saying that there’s not opportunity in traditional business sectors. Of course there is and smart operators will always find a way to offer value to their end customers, but I think that there has been a seismic shift in demand for the digital economy. And of course the digital economy is super broad, and that’s not to say that the hybrid economy can’t also exist, which we’re seeing a lot of too.

Blake Hutchison:

On Flippa, David, it’s interesting. We have unique insight because we see just over 10 million keyword searches on Flippa each month. And so what those individuals are doing is they’re looking for asset types or asset categories. And as a result, we’re able to pull that data each month and compare shifts in search volume month to month or quarter to quarter or annually.

Blake Hutchison:

Now right now, there’s a lot of people who are very excited and for the very first time looking at either setting up or acquiring an asset, which is attached at the hip inextricably connected to the Amazon ecosystem. And that could be that it’s an FBA business, fulfilled by Amazon. It could be that it’s part of the Amazon Associates Program, which is their affiliate program typically used by content assets online. It could be that it’s a publisher using the Amazon Kindle or Amazon Publishing services program for the first time. But Amazon is our second largest keyword search on Flippa right now. And that’s an ongoing shift, but it’s different to what we saw, say 12 months back.

Blake Hutchison:

In addition to that, I associate with some of the comments you made very early on in your talk about categories that are seeing strong growth right now. So fitness is in our top 10 searches. Now think about that. 10 million searches a month. It’s in our top 10. Music is in our top 10. Health is in our top 10. And then the rest I would say are more our business models. So AdSense, blog, advertising, SEO, those types of things. So it is super interesting.

David Nilssen:

Yeah. Cool.

Benjamin Weiss:

And that’s great stuff. Guys, it’s been about 40 minutes, so I know we do have a few questions left, so I might just have to leave David and Blake with a little bit of homework and I’ll send these questions to them. We’ll get them answered in writing and we will post these, I know at least on the Flippa blog and we’ll probably get some information out on the Guidant side as well, but I will let these gentlemen get on with their day. And I know you all have plenty of thinking to do about where you’re going to be investing your money and how you’re going to be investing it and how you’re going to be financing it, might say. So thank you, David. Thank you, Blake. This has been absolutely fantastic. I think we all learned a lot about both sides of this equation. Thank you everyone for attending and we hope to hear from you soon. Cheers guys.

David Nilssen:

Thank you.

Benjamin Weiss is a marketing all-star at Flippa. He has well over a decade of experience running multifaceted marketing programs within the CPG industry and knows just what it takes to drive a business from vision to reality. You will often find him enjoying a cold beer on a hot day in Austin, TX, or you can always find him on LinkedIn.

Success Stories

Built. Scaled. Exited with Flippa

Hear from business owners and entrepreneurs who have bought and sold online businesses on Flippa.

Calculate your repayments and returns with Flippa’s seller financing tool.

Keep up with the latest from Flippa

Subscribe to our blog and get free tips, advice, and resources delivered directly to your inbox.

Need Help?

We understand that buying or selling a digital business isn’t easy. If you have any questions or require assistance, feel free to contact us anytime.

Contact Customer Support

Search our knowledge base for answers to common questions.